Use your Credit card to boost your credit score – life hack to boost credit score

Table of Contents

The most important is how you manage and use your credit card. You should never be late to pay your credit card bill. Use the online payment option to manage and set your bill payment automatically. Always spend less than you earn. For this, you need a budget that you should follow strictly. Now we going to discuss some tricks that will help you to boost your score tremendously.

Tricks To increase your credit Limit quickly

Only spending six percent of your available credit makes it difficult to gain credit increases from your credit card companies. Because they’re not going to raise your limits on a card you never use.

So, I use this credit score hack to boost my credit scores into the stratosphere. And also you can have massive success with it too!

What I do is charge and maintain a high balance on each card for two months. In the third month, I pay it all off and let it sit for two months. This way, I’m using my credit card enough for the bank. So the bank also continues raising my limit (thus raising my available credit). And at the same time, I am maintaining enough available credit to keep the credit agencies happy.

Master this method, and you’ll notice your score go within months. And there are a few more insider loopholes to instantly transform your life. All these tricks have the tremendous potential to increase your credit score that is already been proven.

Pre-Due Date Payments – A Trick To Boost The Credit Utilization: A Powerful Life Hack to boost credit score

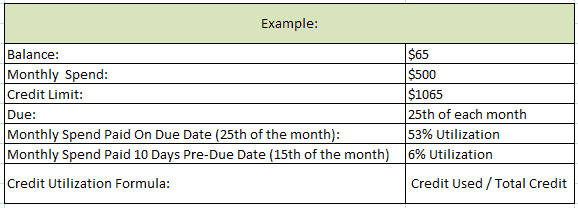

One trick to boost the credit utilization piece of your score without really having to change your spending behavior is to pay your bill approximately 10 days before your due date.

Credit Utilization Formula: Credit Used / Total Credit

Credit Bumpers – a trick to Protect Credit History

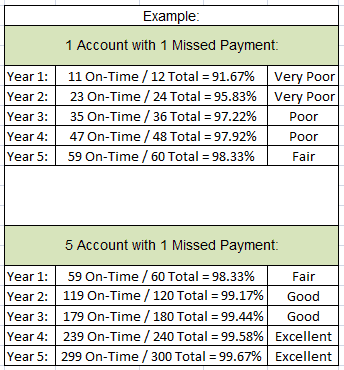

Example:

Just one late payment that happened years ago, maybe when you were back in college, could significantly impact your score today. Therefore one trick to absorb some of the impacts of a negative on your Credit History is to use Credit Bumpers by adding more Accounts to your total number of Open Accounts. This example shows how much faster you recover from one late payment when you have 5 open accounts instead of just one.

Credit History Formula: On-Time Payments / Total Number of Payments

{kind=link}

0 Comments