Do you need LIC insurance policies?

Table of Contents

My motive is not to demotivate you from investing in LIC or any other policies but to encourage you to invest, the only motive is your investment decision should be an informed decision, It should not be like your friends colleagues or family member tells you about the LIC policies that your neighbor took last month and You jump in and purchase the policies.

You should not compare LIC insurance with MF or PPF. It advises not to mix insurance with investment; do not confuse endowment as an investment. It advocates Term Insurance for insurance and MF for investment. And then it goes on to prove how the advised route will yield better returns. Till now I am not talking about whether lic is good or bad. I am trying to give you the actual facts.

Think logically, I am trying to encourage you to grab the best outcome for your investment that you are already invested in or plan to invest that’s why you are spending your time reading this blog. It is your money, and your time so why you have not deserved more when there is a possibility, the only thing is you need a little bit more information and research work on your part.

Pros: LIC is a huge organization, with huge funds. It has been in India since the 50s. At that time, LIC policies were the only method to get life insurance and get returns. LIC used to invest part(a very large part) of our premium into the stock market and then return some part (a small part) of the profits to us at maturity.

The LIC repayment and settlement were always prompt. Thousands took LIC policies for the double benefit – insurance and saving. In fact, the LIC tagline changed to – Beema Bhi, nivesh Bhi (get insurance, get savings). LIC returns are tax-free except for pension schemes.

Cons: LIC is very poor on both counts – life insurance as well as investment. First, life cover by LIC from 5 lakhs to 30 lakhs is too little. You can of course opt for more cover but the premium will be very high. Secondly, the investment return is very poor. At best the return is 6.5%.

LIC is good or bad! Why is LIC Very Attractive to All?

a) LIC promises an assured or guaranteed return and they show an amount that will be paid out to you at maturity (usually between 20 and 30 years). This amount sounds like a FANTASTIC AMOUNT at the present time.

b) LIC keeps harping you on the fact that this money is assured. If one brings up market-linked investment, the argument against always is: Sir, market ka kya bharosa? Aaj hai, Kal Nahi? Aapko Vahan koi guarantee data hai kya? (Sir, what is the assurance of the market? Today it is high, tomorrow not so. Can anyone guarantee market returns?)

c) LIC never ever declares the returns in CAGR terms. Hence we remain ignorant.

d) We hear that neighbor, colleague, a family member purchased a so-and-so LIC policy and we are also immediately concerned – I must have life cover also.

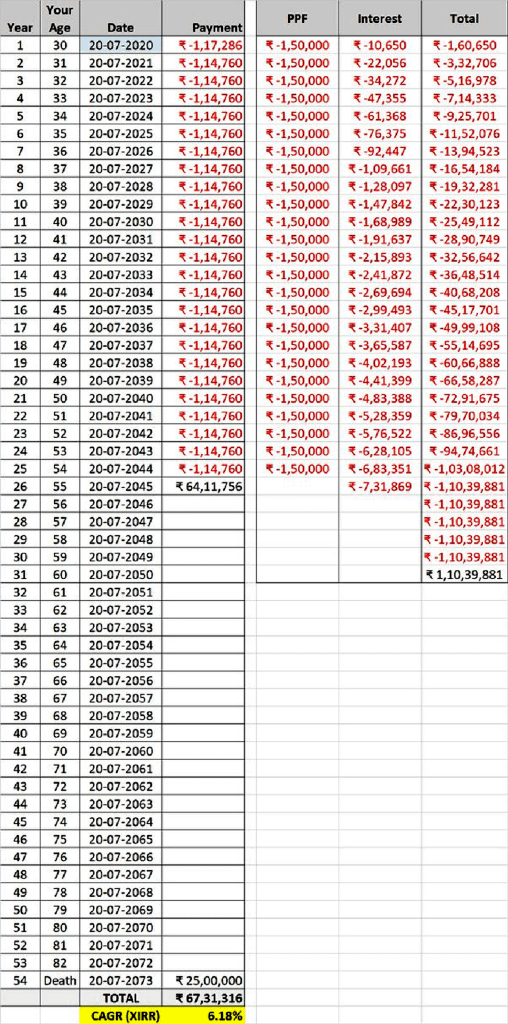

So let us compare the LIC Jeevan Anand 915 policy (the 815 is closed now). The policy sum assured is an example but the rest of the figures are based on this amount with realistic figures:

[A] Sum assured: ₹25,00,000

[B] Term years: 25

[C] Age at the start: 30

D] Policy begins in a year: 2020

[E] Premium per ₹1,00,000: ₹4,581

[F] Rebate on the premium (2%): ₹-91.62

[G] Final Premium per ₹1000: ₹4,489.38

[H] Premium per year: ₹1,12,234.50

[I.1] Premium for the first year @ 4.5% GST: ₹1,17,285.05

[I.2] Premium paid for next 24 years @2.25% GST: ₹1,14,759.78

[J] Total Premium Paid for full-term: ₹28,71,519.68

[K] 125% of total premium: ₹32,26,741.88

[L] Simple Reversionary Bonus rate per ₹1000 of SA (A): ₹49.00

[M] Simple Reversionary Bonus Amount for 25 years (A/1000 * L): ₹30,62,500

[N] Additional Bonus (considered at the same rate for the final year or M): ₹1,22,500

[O] Final Benefit (Greater of A or K+M+N): ₹64,11,756

[P] Payment upon death after maturity: Sum assured = ₹25,00,000

What is the CAGR or return on investment?

- If you consider the full double benefit or O and P, it is a grand 6.53%!

- If you don’t consider (P) because of the “what is the use of this money after my death?” reason, then it is 6.02%

- Have you considered the value of rupees 64,11,756 after 25 years, assuming you enroll in the policy today? It is rupees14,52,263.67. It is still not bad but not grand as it looked, does it?

How is LIC Became Popular

Till the mid-eighties, the stock market was just a steady performer. There was very little buoyancy. There were only a few stock exchanges – just four (BSE, DSE, CSE, and MSE) and some branches. You had to trade physically and via a broker. One did not understand markets – even today also very few do understand.

Then Harshad Mehta scammed his way to dizzy heights. This caused great interest in the stock market as well as scarred people who lost money. LIC remained a winner. Mutual Funds were unknown till the late 90s and only became popular when SIP was introduced. On top of that, there was no term insurance (or LIC never promoted that) and there were no independent private insurance players. Hence LIC reigned like a king.

Today LIC tactics are changed. The argument from all LIC employees and agents is – long-established, always settled (the actual settlement ratio is 98%), trust over the years, government-backed – will not run away with your money, will not fail, etc.

But the biggest argument against Term Insurance by these people is – you are paying all this money but not getting anything in return. Nobody, repeat, nobody gives the real comparison.

So, the alternative?

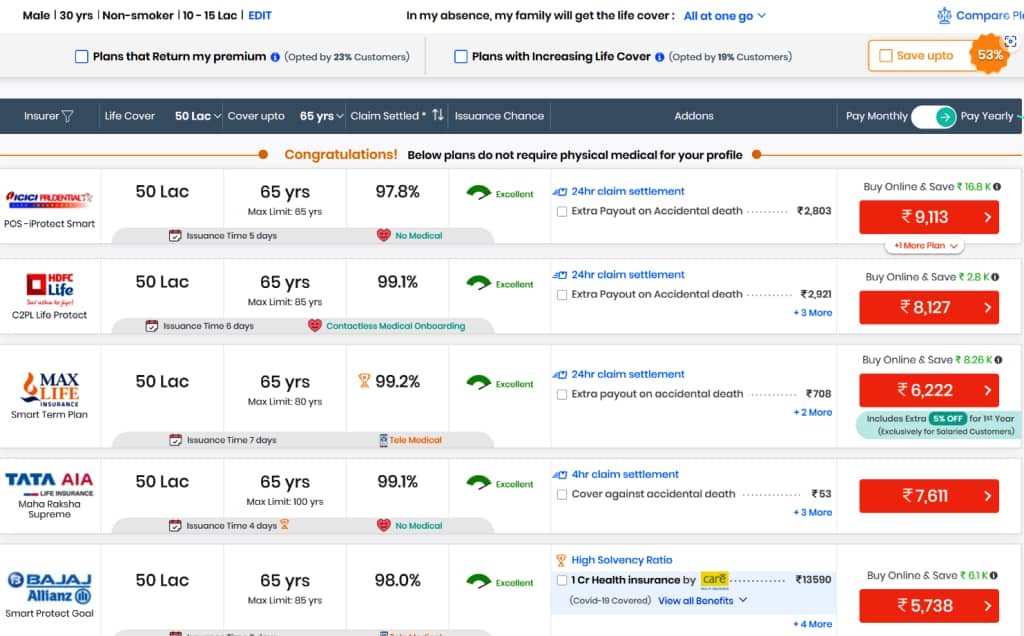

a) A Term Insurance plan of ₹50 lakhs or more. The premium will be much cheaper. See examples at the end.

b) Invest the balance of premium in MFs and get much better returns.

Is lic good or bad?

Comparison: LIC is good or mutual fund in Return Prospective

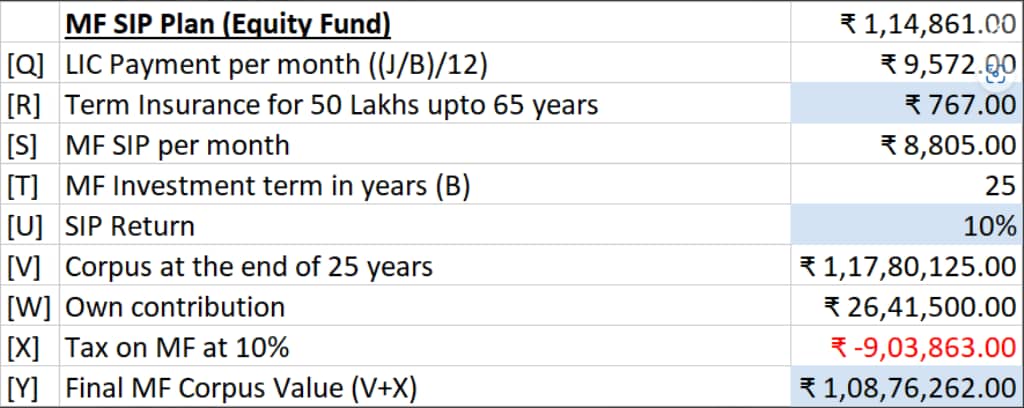

a) For a LIC premium of ₹9,572 per month or ₹1,14,861 per year, you are getting a paltry ₹25 lakhs cover. For ₹12,000 to ₹14,000, the same 30 years old, a non-smoker person can get a ₹1 Cr cover. For as low as ₹778 pm or ₹9336 pa, you will get twice the cover of LIC or ₹50 lakhs.

b) One will be quick to jump, what about returns? So here is a comparison with investing in MF SIP

[Q] LIC Payment per month ((J/B)/12): ₹ 9,572

[R] Term Insurance for 50 Lakhs up to 65 years: ₹ 778

[S] MF SIP per month: ₹ 8,794

[T] MF Investment term in years (B): 25

[U] SIP Return: 10%

[V] Corpus at the end of 25 years: ₹ 1,17,65,408

[W] Own contribution: ₹ 26,38,200

[X] LTCG Tax on MF at 10%: ₹ -9,03,863

[Y] Final MF Corpus Value (V+X): ₹ 1,08,76,262

[Z] Difference (Y-O): ₹ 44,64,506. (I am not considering Death Benefit here because it is of no use to me. Even if I did, it is ₹ 19,64,506 more and lest one forgets, if the MF corpus is untouched, assuming 25 years of vesting, it will grow to ₹ 12,76,34,190.)

Is lic good for long term investment What if you put your money in PPF

c) Do You think MF is risky? Then try PPF. The limit is ₹ 1.5 lakhs per year. But by investing for the same 25 years, you will get₹1,10,39,881. But this assumes a 7.1% constant maturity yield and that can change. Still, it is unlikely to come down to less than 6.5%. And this amount is tax-free also.

Here is the table:

So there is the same cover for you as LIC Jeevan Anand but much much better in respect of more life cover and more return.

LIC-JA-and-MF-Comparison

Is lic a good investment?

Now it’s time to make a decision, look at the numbers above, Twice the life cover and ₹ 44,64,506 more than LIC. With the same amount of money, you are able to get double the benefit and better returns. Is this even comparable? Some will be quick to jump that 10% returns are not possible in MF. I will simply say – please go and re-examine. It is quite possible and in fact, I have achieved higher results of 12.75% since Nov-2007.

In the last 5 years, I have achieved 22.13%. 10% is very-very modest and completely possible as long as you do a little bit of research on your part, select the right funds, keep monitoring returns, and take remedial actions like switching. Markets rise and fall but over a long term of 25 years, you will always get a pretty decent return because of the power of compounding and hedging, and averaging due to SIP. I can promise this at least based on my own experience.

One USP about LIC is that it allows loans on the policy. Hogwash! The loan amount is 90% of the policy surrender value at the time of the loan, not the sum assured. The policy does not allow getting benefits early. If you wanted early benefits, the only way is to surrender the policy completely. With MF, you can dip into the corpus at any time. No need for a loan.

Few things to know about LIC:

- GOI has nothing to do with this (LIC policies). LIC is an independent company having its own legal status, chairman, MD, board of directors, etc. Government happens to be the majority shareholder. The GOI does not tell LIC which policies to issue and what should be the T&C, returns, etc. LIC does that. GOI interferes with some other things regarding employment guarantees, reservations, promotion policy, etc.

- LIC policies are not bogus. They offer what they say they will offer. There is indeed a guaranteed return. It is just that the returns are low.

- Agents do not tell you the whole truth. It is the LIC agents who are at fault. Perhaps they are also a misapprehension. But the fact is that the agent tells you and sells you a dream. We are duped by the dream. However, the dupe is not to understand the effect of inflation. So we are equally at fault for purchasing something on a promise and not understanding the product correctly.

Check the cost for Term insurance for 50 laks (min offered by most) and used in the calculation above:

0 Comments